The concept of borrowing against your assets and equity you already own, has been around for a very long time. The classic example is taking debt against a home you have equity in. Thus, the bank holds your house as collateral and gives you a loan in return. This concept of leverage has been forming its place in the world of cryptocurrency and digital assets for a few years now.

Understanding the tax implications of this is vital before taking on any significant loans against your crypto holdings. It is recommended to consult with a crypto accountant or a crypto CPA for better understanding on this topic. Let’s dive into taxation of crypto loans, tax planning strategies, and the pros and cons of taking a loan against your crypto assets.

borrowing against Bitcoin What is a crypto loan?

A crypto loan is a secured loan that uses your cryptocurrency such as BTC or ETH as collateral in exchange for liquidity from a lender. The lender can typically give you fiat as a loan (i.e. USD, Euro) or can even give you crypto as a loan (i.e. ETH, Litecoin). Some lenders provide stablecoins as a loan (i.e. USDC, USDT) and others offer fiat and crypto. Installment payments are then made to the lender and as long as you repay the loan amount in full and cover any interest, you will get your original assets back at the end of the loan term.

The amount that is lent to you is always a percentage of the value of the cryptocurrency at that time, which is called a loan-to-value ratio. So if BTC is trading at $40,000 and you have 10 bitcoins that you’d like to take a loan against, you’d be putting up $400,000 as collateral. If you then need a loan of, let’s say, $100,000, you would be receiving a LTV of 25%.

| Asset |

Amount |

Market Value | Total Value | Loan Amount | LTV |

| BTC | 10 | $40,000 | $400,000 | $100,000 | 25% |

| ETH | 50 | $2,000 | $100,000 | $40,000 | 40% |

Loan terms vary and can sometimes be up to 5 or 10 years with APRs typically below 12%. Again, it all depends on who the lender is and whether or not it is a centralized exchange or lender, or if it is a decentralized lender like Aave.

What are different types of lenders borrowing against Bitcoin?

Two different types of lenders can be CeFi lenders and DeFi lenders.

- Centralized Finance (CeFi) loans are loans where the lender actually holds custody of your assets during the repayment period. You would then be unable to do anything with those assets until the loan is satisfied and repaid or canceled.

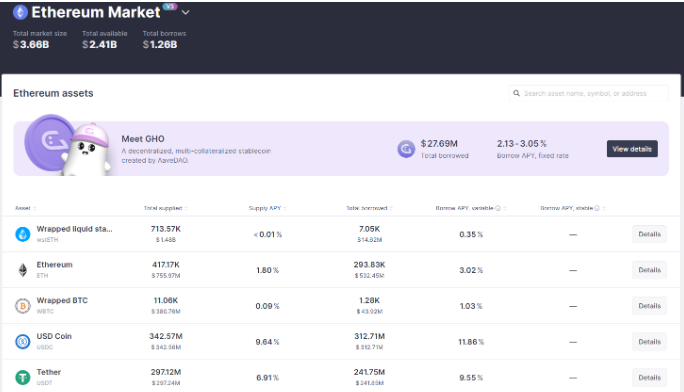

- Decentralized Finance (DeFi) loans work based on smart contracts that are pre-determined and set by code. For example, you can go to Aave (https://aave.com/) and put your Ethereum as collateral and receive an LTV of 80% at the time of writing this article.

Here’s a snapshot of Aave showing the Supply APY for ETH at 1.80% and the borrow APY for ETH at 3.02%.

What are the benefits and risks of taking a crypto loan?

There are a lot of positives when it comes to taking on a crypto loan. The most beneficial aspect is the ability to quickly get funded and easily payback the loan when desired. This makes it a far more fluid process versus traditional means. When it comes to traditional lending and borrowing, there tends to be a longer review process and restrictions as it comes to paying the loan back early. This doesn’t tend to be the case when borrowing on a DeFi platform such as Aave.

Additionally, when it comes to rates, you are usually paying far less interest than if you were to go get a personal loan through a bank or alternative lending institution. If you are planning to hold your crypto and keep your exposure to the volatility and fluctuations in price – a crypto loan could be a great way to access quick and easy financing.

However, while it is simpler than going into a branch and submitting an application, you are also taking far more counterparty risk. If you go to a CeFi lending institution, your holdings are not as secure as if you were to go to a big bank like JP Morgan Chase, Bank of America, or Citibank.

Additionally, there is risk associated with a volatile underlying. If you receive financing through a bank for a mortgage for example, the price of the home is not fluctuating 20-50% at times. In the world of cryptocurrency, whether it is Bitcoin or an alternative asset, these tokens tend to fluctuate non-stop. This could put you at risk of collateral liquidation if your underlying assets tanks in price and your LTV ratio is not properly maintained.

| Benefits | Risk |

| Duration and payback is flexible | If LTV goes above your threshold you will need to add additional collateral |

| Use agnostic | DeFi platforms can auto-liquidate you if a threshold his crossed |

| Quicker funding than traditional methods | Borrower risks losing their holdings if the lender goes belly up |

| No credit check needed | Volatility in prices of your holdings can move your LTV up and down quickly |

| Interest rates are relatively lower | Depending on the lender there could be little to no KYC done on the borrower |

| No need to sell your crypto holdings | No access to your holdings when it is held with a CeFi lender |

Taxation of crypto loans borrowing against Bitcoin

Income Tax Considerations

Crypto loans are generally not considered taxable income as are most loans in most cases. Tax authorities in the United States are still forming regulations around cryptocurrencies and therefore it would be wise to consult with a crypto accounting firm or crypto tax accountant prior to taking on any sizable loans and posting collateral. A crypto accountant or a crypto accounting firm such as OnChain Accounting (onchainaccounting.com), would be a great starting point for accumulating such information.

Borrowing against Bitcoin or Ethereum can affect the holding period of your assets for tax purposes. Generally, when using your collateral for a loan, your holding period will reset. This is important because it can affect the tax rate you end up paying for that underlying asset’s capital gains. The threshold for long-term vs short-term capital gains bitcoin tax is 1 year.

Therefore, if you post your Bitcoin as collateral prior to holding it for a year, and it goes up in value since you purchased the asset, you will likely pay short-term capital gains tax, which is a far higher percentage than long-term capital gains tax. Sometimes the difference could be as much as 20%!

Strategic tax planning with a crypto CPA can significantly change the outcome of your financial picture. It is imperative to understand the changes in bitcoin tax rates and capital gains tax and how it could affect your tax liability when taking on a crypto loan borrowing against Bitcoin.

borrowing against Bitcoin

When it comes to deducting the interest paid on crypto loans, it’s essential to understand the eligibility criteria set forth by tax authorities. This knowledge can help borrowers optimize their tax situations and reduce their overall liability. To be eligible for interest deductions, borrowers must consider several factors. Firstly, the primary purpose of the loan should be for investments or business activities.

Borrowers should be able to demonstrate that the funds were used for income-generating or productive purposes, such as expanding a business or investing in appreciating assets. Proper documentation is crucial. Maintaining comprehensive records of the loan, including the loan agreement, transaction history, and the specific use of funds, is vital to substantiate the deduction claim and provide evidence in case of an audit. Furthermore, the interest paid on the crypto loan must be in cash or its equivalent; in-kind interest payments, such as paying interest with additional cryptocurrency, may not qualify for deductions. It’s advisable to use cash payments to ensure eligibility.

Additionally, full tax compliance is essential, including accurate reporting of the loan and interest payments on tax returns, as failing to do so could jeopardize eligibility for deductions and lead to penalties borrowing against Bitcoin.

While interest deductions can offer valuable tax benefits for borrowers, there are limitations and considerations to keep in mind. The IRS may impose debt limits on interest deductions, and borrowers should be aware of any applicable limits, which can vary depending on the type of loan and the use of funds. Exceeding these limits may borrowing against Bitcoin result in reduced or disallowed deductions borrowing against Bitcoin.

It’s crucial to distinguish between personal and investment use of loan proceeds, as interest deductions are generally available for investments and business activities but may not apply to personal expenses. Clear documentation of how the funds were used is essential to support deductions. Moreover, the timing of deductions can often be claimed in the tax year in which the interest is paid, but specific rules may apply, and borrowers should consult tax professionals for guidance on timing deductions optimally. Lastly, borrowers should stay informed about changing tax laws and regulations that may affect their ability to claim interest deductions borrowing against Bitcoin.

Consulting with tax professionals can help navigate evolving tax landscapes. By understanding these eligibility criteria, limitations, and considerations surrounding interest deductions for crypto loans, borrowers can make informed decisions, maximize tax benefits, and ensure compliance with tax laws while optimizing their financial strategies borrowing against Bitcoin.

Should I take on a crypto loan as leverage?

Assessing the risks and benefits of taking on a crypto loan is imperative. It could be an extremely useful tool as it is liquidity that is easy to access and quick to receive. However, ignoring the underlying asset price of your collateral or working with a CeFi lender who is not reputable, can increase your risk borrowing against Bitcoin!

Start with asking yourself why you are taking this loan on and do a cost benefit analysis. Are you able to receive a similar loan at a similar rate elsewhere? How does the rate you would be getting, compare to other lenders or traditional financing? How long do you plan on holding this loan for? How long have you been holding the underlying assets for that you will be posting as collateral?

If you can avoid paying short-term capital gains, you should do whatever necessary to do that as the tax consequences could be far greater than if you paid long term capital gains tax. This is a great discussion to have with your crypto CPA!

Additional resources

OnChain Accounting is a great resource for your crypto tax questions. They have extensive experience with companies and individuals who are operating on-chain and are borrowing and lending in the crypto space. Email them for a free consultation to discuss any crypto tax strategies you may be interested in.

An additional resource that could be of great help is following FASB’s news related to crypto. There is constant guidance being provided by tax authorities in the US and each year that passes, there is more regulation in the space. Remaining up to date with this news is extremely important as new developments could impact your financial decisions borrowing against Bitcoin!